Lets go back to the start of the COVID crises;

- Businesses suffered huge losses

- People started losing their jobs

- Demand for everything dropped (low inflation) &

- The economy was at a standstill.

What could have been done to revive the economy?

As a central bank, the easiest way to ride through a crises of Low demand/inflation is,

- Reducing interest rates &/or

- Increasing liquidity in the market

How do you increase liquidity?

Central banks issue bonds in which banks invest. That’s the way central banks suck liquidity from the banks & give them bonds. When they want to infuse liquidity, they do the opposite; they buy back the bonds & give banks money/liquidity

By reducing rates or increasing liquidity in the market, you are trying to,

- Create demand

- Save job losses &

- Keep the economy running.

How?

(a) For individuals – Assumption is that when rates are low, they will take a loan and buy a Laptop, car, house etc. there by increasing the demand

(b) For corporates – Assumption is that when rates are low, they will borrow money and do CAPEX and hence demand up

When Corona hit, rates were reduced globally & liquidity was infused in the system. Rates in US were down to close to Zero.

Would you invest in fixed income if you are going to make close to zero interest? No & hence this money started getting invested in Equity & Gold

Where did they get the money from in such crises you may ask?

(a) Individuals – Got unemployment benefits

(b) Corporates – Could borrow at close to zero

(c) Financial institutions – Were flooded with money because central banks were buying bonds & infusing liquidity

Along with investing in the US equities, a lot of investment was done in emerging markets as well.

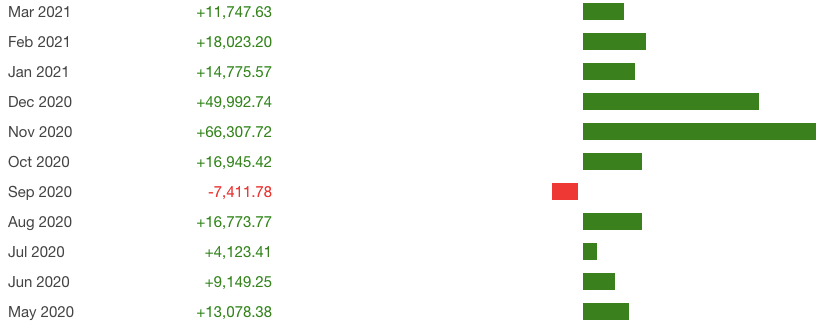

Below is the FII data of investments in India and the values are in cr.

Essentially, rates were close to zero and hence there was no interest in investing in fixed income & hence investment happened in Equities globally and why we saw the equity markets recover so swiftly in 2020 – 2021, liquidity driven rally!

What’s happening right now?

-Job market has recovered, there is less unemployment

-Businesses are back to pre covid or doing even better

-Demand & hence inflation is back

So if things are back to pre covid, do we still need the incentive of lower rates & more liquidity? Probably not.

Also higher inflation has been a major reason why elections are lost & hence it’s in the interest of the government also to keep the inflation low

Hence the US Fed has decided to,

- Reduce the bond-buying program and end it by June and also

- Start raising rates soon after that. The expectation is 3-4 rate hikes the next year

Why is this hurting the market?

(1) If rates go up, fixed income investing is easier to do

(2) If rates go up & liquidity reduces, there will be less easy money available for investing in risk assets

(3) If rates go up, loans become expensive & hence it hurts demand (opposite of the laptop, car & house example)

(4) Most importantly, valuation.

Example:

One way of valuing stock is using the DCF method.

- You project the future cash flows of the business for the coming 3-5 years & discount it at a particular rate to arrive at today’s value of the business

Lets say for example,

Expected Cash Flow of the business,

Year 1 – 1000

Year 2 – 1400

Year 3 – 2000

If I discount it at 6%, today’s value of the business is 3,868 but if rates increases & I discount it at 8% the value drops to 3713

Valuation drops in a rising rate market if the company is not able to out perform on the expected earnings

Which is why you see NASDAQ falling more than the S&P.

- NASDAQ has higher growth stocks expected to have larger future earnings & hence trading at premium valuations.

- If rates go up & stock are not able to out perform their expected earnings, stocks will fall

Anticipating the liquidity reduction & rate hikes, FII’s have been selling relentlessly & why our markets have been under pressure for the last 2 months now